Thinking about updating the floors in your business space? It might seem like just a cosmetic change, but guess what? It could actually save you money on your taxes. We’re talking about capital allowances, and for 2026, there are some things you should know about getting tax relief for commercial flooring upgrades. It’s not as complicated as it sounds, and a little planning can go a long way.

Key Takeaways

- Upgrading your business floors can lead to tax savings through capital allowances.

- Capital allowances let you deduct the cost of certain business assets from your profits.

- New rules in 2026 might affect how you claim these allowances for flooring.

- Not all flooring expenses qualify, so check what counts as a business improvement.

- Good record-keeping and talking to a tax pro will help you get the most commercial flooring tax relief.

Unlocking Tax Savings With Commercial Flooring Upgrades

Why Flooring Matters for Your Business Taxes

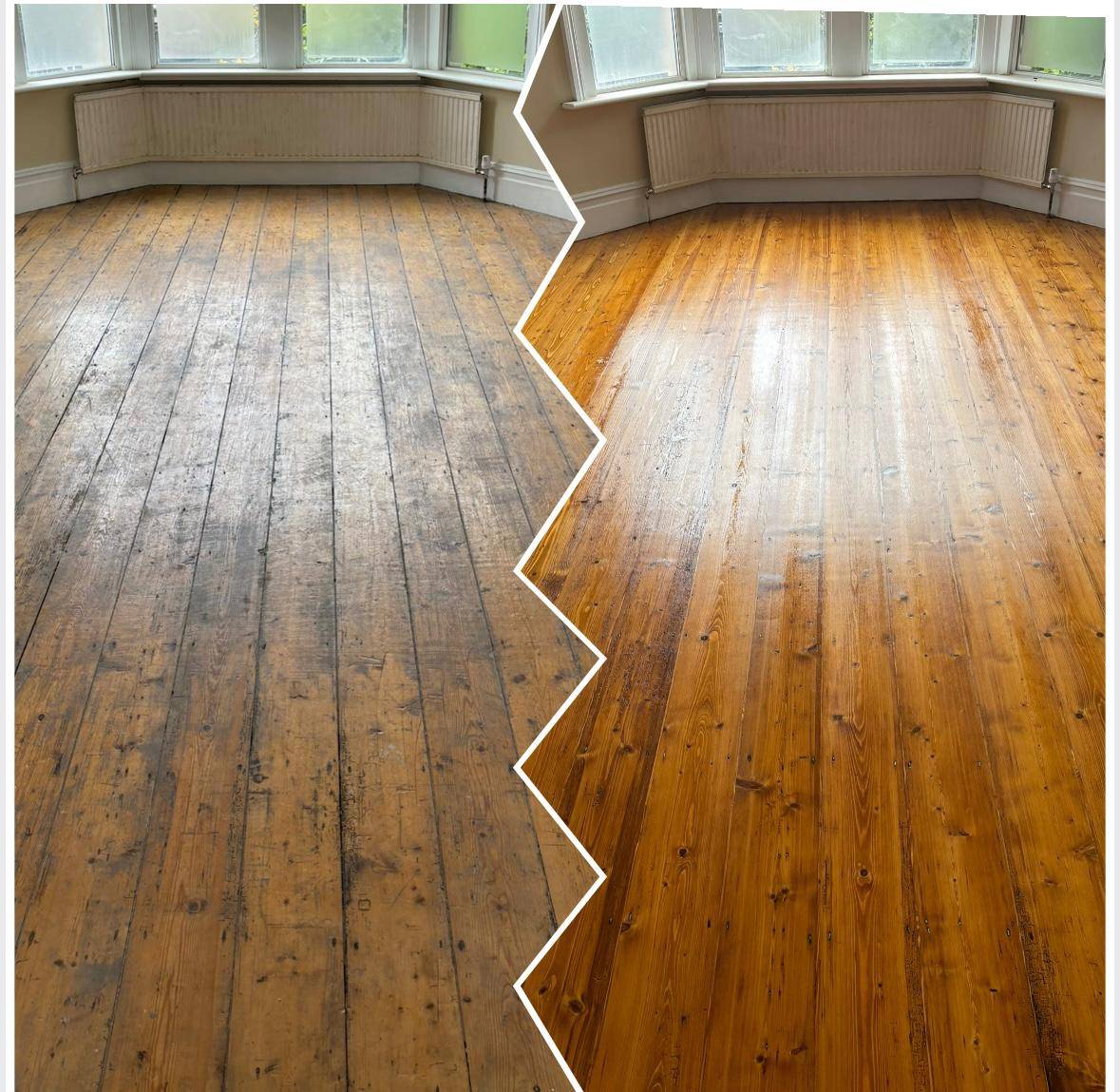

So, you’re thinking about sprucing up the office floors? Maybe the old carpet is looking a bit sad, or perhaps you’re going for a more modern look with some slick LVT. Well, guess what? That flooring upgrade might be doing more for your business than just making the place look good. It could actually be a smart move for your taxes. It’s not just about aesthetics; it’s about smart business spending.

Think about it. When you invest in your business property, especially things that are built-in or part of the structure, the taxman often lets you write off a portion of that cost over time. This is where capital allowances come into play. For flooring, this means that the money you spend on new, qualifying materials and installation could lead to a nice tax deduction down the line. It’s a way for the government to encourage businesses to invest and improve their premises.

The Big Picture: Commercial Flooring Tax Relief Explained

Basically, tax relief on commercial flooring is all about reducing your taxable income. Instead of just paying taxes on all your profits, you get to subtract certain business expenses. Capital allowances are a specific type of deduction that applies to assets you use in your business for a long time, like, well, your floors! Instead of deducting the whole cost in one go (which you usually can’t do for big purchases), you spread it out over several years. This can really help manage your tax bill, especially in the year you make the upgrade and the years that follow.

Here’s a quick rundown of how it generally works:

- You spend money: You buy new flooring and pay for its installation.

- It qualifies: The flooring and installation meet the criteria for capital allowances.

- You claim: You work with your accountant to claim these allowances on your tax return.

- You save: Your taxable profit goes down, meaning you pay less tax.

The key is understanding what counts. Not every little thing you do to your office will qualify for these kinds of tax breaks. It’s usually about significant improvements or additions that become part of the property itself. So, getting the details right is pretty important if you want to see those savings.

It might seem a bit complicated at first, but understanding these allowances can make a real difference to your bottom line. It’s like finding money you didn’t know you had, just by making a sensible business decision about your workspace.

Navigating the Capital Allowances Landscape

Okay, so we’ve talked about why upgrading your business floors can be a smart move tax-wise. Now, let’s get into the nitty-gritty of how that actually works. It all comes down to something called capital allowances.

What Are Capital Allowances, Anyway?

Think of capital allowances as the taxman’s way of letting you claim back some of the cost of business assets over time. Instead of trying to deduct the whole expense in one go (which is usually only for smaller, everyday costs), you spread the deduction out. For bigger purchases, like that fancy new flooring you’re planning, capital allowances are the ticket. They’re basically a tax deduction for the wear and tear or obsolescence of your business assets. It’s a way for the government to encourage businesses to invest in their premises and equipment. It’s not a refund, mind you, but a reduction in your taxable profit, which means you pay less tax overall.

Key Changes Coming in 2026 for Businesses

Now, here’s where things get interesting for 2026. The government is tweaking the rules around capital allowances, and it’s good to be aware of what’s changing, especially for things like flooring. While the specifics can get complicated, the general idea is to keep things relatively straightforward for businesses.

Here’s a quick rundown of what you might see:

- Annual Investment Allowance (AIA): This is a big one. The AIA lets you deduct the full cost of qualifying plant and machinery (and sometimes other assets) from your profits, up to a certain limit, in the year you buy them. Keep an eye on the AIA limit for 2026, as it can change. It’s often the easiest way to get a significant tax break.

- Writing Down Allowances (WDAs): If your flooring costs are more than the AIA limit, or if they don’t qualify for AIA, you’ll likely use WDAs. These are calculated as a percentage of the asset’s value each year. There are different rates depending on the type of asset.

- Specific Flooring Rules: While flooring is often considered part of the building, certain types of commercial flooring, especially those that are more like ‘plant’ (think specialised industrial flooring or removable systems), might qualify for different treatment. It really depends on the nature of the flooring and how it’s installed.

The main takeaway here is that the government wants businesses to invest. By offering capital allowances, they’re trying to make it more financially attractive to upgrade your workspace. It’s not just about making your office look nicer; it’s about potentially reducing your tax bill significantly.

It’s always a good idea to chat with your accountant or tax advisor about these changes. They can tell you exactly how the 2026 rules will affect your specific situation and help you figure out the best way to claim what you’re entitled to. Don’t leave money on the table!

Identifying Eligible Flooring Expenses

So, you’re thinking about sprucing up your business floors and wondering if that’s going to save you some cash on taxes. Good question! Not every bit of flooring work will qualify for capital allowances, but a lot of it can. The key is to figure out if the upgrade is considered a ‘plant’ or ‘machinery’ expense by HMRC, or if it’s just part of the building itself.

What Counts as a Qualifying Improvement?

Generally, if your new flooring is something that can be removed without damaging the building, or if it’s part of a larger system that qualifies, you’re in a good spot. Think about things that aren’t permanently fixed into the structure.

Here are some common examples that usually make the cut:

- Specialised commercial carpeting: Especially if it’s installed in a way that it can be taken up later.

- Modular flooring systems: Like interlocking tiles or raised access flooring.

- Resilient flooring: Such as vinyl or rubber flooring that’s glued down but can be replaced without major structural work.

- Epoxy or resin coatings: Applied to concrete floors for specific functional purposes (like in a workshop).

Beyond the Surface: What Else Can You Claim?

It’s not just the flooring material itself. You might be able to claim for other related costs too. This is where it gets a bit more detailed, but it’s worth looking into.

- Preparation work: This could include things like levelling the subfloor or removing old, unsuitable flooring if it’s directly tied to installing the new qualifying flooring.

- Installation costs: The actual labour involved in fitting the new flooring.

- Associated fixtures: Sometimes, if the flooring is part of a bigger setup, like a dance floor with integrated lighting, those elements might also be claimable.

Remember, the goal is to distinguish between improvements that are part of the building’s fabric and those that are more like equipment or fixtures that serve a specific business purpose. If it’s something you could, in theory, take with you if you moved premises (even if it’s a hassle), it’s more likely to qualify.

It’s a bit of a grey area sometimes, so if you’re unsure, it’s always best to chat with your accountant or a tax advisor. They can help you sort out exactly what you can and can’t claim for your specific situation.

Maximising Your Commercial Flooring Tax Relief

So, you’ve decided to upgrade your business floors, and you’re looking at the tax breaks. That’s smart! Getting the most out of capital allowances isn’t just about knowing the rules; it’s about playing it smart. Let’s talk about how to make sure you’re not leaving any money on the table.

Strategic Planning for Maximum Deductions

Thinking ahead is key here. Don’t just slap down some new carpet and hope for the best tax-wise. You need a plan. This means understanding what qualifies before you sign any contracts. For instance, if you’re just replacing worn-out tiles with the exact same kind, that might not count as a significant improvement. But if you’re upgrading to something more durable, energy-efficient, or that meets new accessibility standards, you’re likely in a better position to claim.

Here’s a quick rundown of things to consider when planning:

- Timing is Everything: When do you plan to do the upgrade? Doing it near the end of your financial year might mean you can claim the allowance sooner. Talk to your accountant about the best time to incur the expense.

- Scope of Work: What exactly are you doing? Is it a full rip-out and replacement, or just a refresh? The more substantial the improvement, the more likely it is to qualify for capital allowances.

- Documentation: Keep everything. Every invoice, receipt, contract, and even photos of the old flooring and the new installation. This is your proof.

- Future Needs: Think about how your business might grow or change. Installing flooring that can adapt to future needs might be a better long-term investment and could also strengthen your claim.

Working With Your Tax Professional

Look, tax stuff can get complicated, and flooring is no exception. Trying to figure it all out yourself is a recipe for headaches, and honestly, you might miss out on savings. Your tax advisor is your best friend when it comes to capital allowances. They know the ins and outs of the tax code and can help you structure your flooring project to get the biggest tax benefit.

Here’s what they can help with:

- Identifying Qualifying Expenses: They can tell you definitively what parts of your flooring project are eligible for capital allowances.

- Calculating Your Claim: They’ll do the math to figure out the exact amount you can claim.

- Navigating the Paperwork: They handle the forms and ensure everything is filed correctly with HMRC.

- Advising on Timing: They can help you decide the best time to make the purchase or complete the work to maximise your tax relief.

Don’t be shy about asking questions. A good tax professional will explain things in a way you can understand, even if you’re not a numbers person. They’re there to help your business save money, so use their knowledge!

Remember, the goal is to make smart business decisions that also benefit your bottom line. Upgrading your flooring is a great opportunity to do just that, especially with capital allowances available. Just make sure you’re planning ahead and getting the right advice.

Common Pitfalls to Avoid

Don’t Miss Out on Potential Savings

So, you’re thinking about upgrading your business floors and want to snag those tax breaks. That’s smart! But, it’s super easy to mess this up if you’re not careful. A lot of businesses just don’t claim what they’re owed, and that’s a real shame. It’s like leaving money on the table. We’ve seen folks overlook simple things that could have saved them a good chunk of change. The biggest mistake? Just not knowing what you can actually claim. It’s not always obvious, and the rules can feel a bit like a maze.

Keeping Accurate Records is Key

This is where things can get messy. If you don’t have solid records, good luck proving your flooring upgrade qualifies for capital allowances. Think about it: the tax folks want to see proof. This means keeping all your invoices, receipts, and any contracts related to the flooring work. Don’t just shove them in a drawer; organise them! A disorganised mess means you might miss out, or worse, get questioned later.

Here’s a quick rundown of what you absolutely need to keep:

- Original Invoices: These should clearly show the cost of the flooring materials and the labor for installation.

- Payment Records: Proof that you actually paid the bills – bank statements or cancelled checks work.

- Project Details: Any notes or plans that describe the scope of the work, especially if it’s part of a larger renovation.

- Dates: Make sure you have the dates of purchase and installation. This is important for timing your claims.

Sometimes, the line between a repair and an improvement can be blurry. If you’re just patching up a small worn spot, that’s probably a repair and not eligible. But if you’re ripping out old carpet and putting in new, durable LVT throughout your main office space? That’s usually a capital improvement and a prime candidate for allowances. Always check the specifics for your situation.

Don’t forget about things that might seem minor but add up. Did you have to move heavy furniture? Was there specialised prep work needed for the subfloor? Sometimes these associated costs can also be factored in. It’s worth digging into the details to see what else might qualify. If you’re unsure, it’s always best to chat with someone who knows this stuff inside and out.

Watch out for common mistakes that can mess up your project. Many people skip important steps or use the wrong tools, leading to problems down the road. Don’t let that happen to you! For expert advice and to see how we can help, visit our website today.

Wrapping It Up

So, that’s the lowdown on capital allowances for your commercial floor upgrades in 2026. It might seem like a lot to sort through, but honestly, getting these tax breaks can really make a difference for your business’s bottom line. Don’t just let this opportunity pass you by. Take a bit of time, maybe chat with an accountant if you’re feeling unsure, and figure out how you can take advantage of these rules. It’s all about making smart moves for your business, and this is definitely one of them. Good luck!

Frequently Asked Questions

So, what exactly are capital allowances?

Think of capital allowances as a way for your business to get a tax break on things you buy to help your business run, like new flooring. Instead of deducting the whole cost at once, you can spread the savings over time. It’s like getting a little bit back from the government each year for your investment.

Will upgrading my office floors save me money on taxes in 2026?

You bet! When you put in new flooring for your business space, it’s often seen as an improvement. This means you can usually claim capital allowances on that cost, which lowers your taxable income. So, yeah, it can definitely help your wallet.

What kind of flooring can I get a tax break on?

Generally, if the flooring is a permanent part of your business building and you bought it to use in your work, it’s likely eligible. This could be anything from sturdy carpet tiles in an office to tough vinyl in a workshop. The main thing is that it’s for your business use.

Are there any specific changes for 2026 I should know about?

While the big rules usually stay similar, it’s always smart to check for any updates closer to 2026. Tax laws can tweak things a bit. Planning ahead and talking to an expert is the best way to catch any new details that might affect your flooring project.

What if I’m not sure if my flooring project qualifies?

No worries! That’s where your tax advisor or accountant comes in. They’re the pros who know all the ins and outs of what counts and what doesn’t. They can help you figure out exactly what you can claim and make sure you don’t miss out on any savings.

How do I make sure I get the most tax savings from my flooring upgrade?

The key is to plan it out. Keep all your receipts and invoices super organised. Knowing what you spent and what it was for makes claiming the allowances much easier. Good records are your best friend when it comes to saving money on taxes!